Minnesota Administrative Rules

7035.2685 COST ESTIMATES FOR CLOSURE, POSTCLOSURE CARE, AND CORRECTIVE ACTION.

Subpart 1.

Cost estimate requirements.

The following provisions apply to cost estimates.

A.

The owner or operator shall make a written estimate, in current dollars, of the cost of closing the facility in accordance with part 7035.2625 and applicable closure requirements in part 7035.2635. The estimate must be calculated according to subitems (1) and (2).

(1)

The closure cost estimate must equal the cost of closure at the point in the facility's operating life when the extent and manner of its operation would make closure the most expensive, as indicated by its closure plan.

(2)

An owner or operator who establishes a trust under part 7035.2705 or 7035.2715 or a dedicated long-term care trust fund under part 7035.2720 may make the closure cost estimate in present value terms, provided that interest earned from investment becomes part of the fund.

The method used to calculate a present value for closure cost estimates must have the following form:

| P = |

F --------- (1 + i)n |

|

| in which: | P = | the present value, |

| F = | the estimated cost of facility closure as calculated under subitem (1), | |

| i = | the interest rate, and | |

| n = | the time period in which the design capacity of the facility is filled, expressed as the number of years after the date on which the cost estimate is made. |

The interest rate used must be the Federal Reserve Bank discount rate in effect at the Federal Reserve Bank in Minneapolis, Minnesota.

B.

The owner or operator of a facility subject to postclosure monitoring or maintenance requirements shall make a written estimate, in current dollars, of the annual cost of monitoring and maintenance of the facility in accordance with the applicable postclosure requirements in part 7035.2645. The estimate must be calculated according to subitems (1) and (2).

(1)

The owner or operator must calculate the postclosure cost estimate by multiplying the annual postclosure cost estimate by the number of years of postclosure care required under part 7035.2655. The postclosure cost estimate must include a contingency element that accounts for inflation expected to occur after site closure.

(2)

An owner or operator who establishes a trust under part 7035.2705 or 7035.2715 or a dedicated long-term care trust fund under part 7035.2720 may make the postclosure cost estimate in present value terms, provided that interest earned from investment becomes part of the fund.

A present value must be reported for each year of the postclosure care period. The time periods used must begin the year after facility closure. The method used to calculate a present value must have the following form:

| P = |

F --------- (1 + i)n |

|

| in which: | P = | the present value, |

| F = | the estimated cost of postclosure care and maintenance during the year in which cost will be incurred as calculated under subitem (1), | |

| i = | the interest rate, and | |

| n = | the time period in which the cost will be incurred, expressed as the number of years after the date on which the cost estimate is made. |

The interest rate used must be the Federal Reserve Bank discount rate in effect at the Federal Reserve Bank in Minneapolis, Minnesota.

C.

The owner or operator shall make a written estimate, in current dollars, of the cost of performing contingency action. The contingency action cost estimate must equal the expected value of implementing the contingency action plan required under part 7035.2615. The owner or operator of a new facility may use method (1) or (2) to calculate the expected value of implementing the contingency action plan. The owner or operator of an existing facility must use method (2) to calculate the expected value of implementing the contingency action plan.

(1)

The expected value may be based on probability analyses unique to the facility. These analyses must determine the probability of occurrence of each event described in the contingency action plan. The expected value of a single event is its implementation cost times its probability of occurrence. The expected value of implementing the entire contingency action plan is the sum of the expected values of each event described in the plan. If an owner or operator chooses this alternative, the owner or operator shall provide the commissioner with details of the cost and probability analyses sufficient to allow the commissioner to evaluate the plan.

(2)

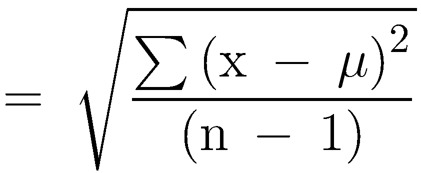

The expected value calculations may assume that the probabilities of occurrence of the events described in the contingency action plan are normally distributed. These calculations will assign probabilities to events according to the following formula:

where f(x) = the probability of occurrence of event x;

µ = the mean (or average) value of the normal random variable x;

= Σx/n;

n = the number of times x is evaluated;

σ = the standard deviation of x;

pi = 3.1416;

e = 2.7183; and

x = a specified dollar interval that controls the number of times x will be evaluated within the range defined by zero and the worst case series of events.

(b)

The probability of the most costly series of events must be at least four times greater than the probability of no contingency action costs.

Subp. 2.

Yearly update of cost estimate.

During the operating life of the facility, the owner or operator shall adjust the cost estimates required in subpart 1 for inflation annually before the anniversary of the date on which the first cost estimates were prepared. The adjustment must be made using an inflation factor derived from the annual Implicit Price Deflator for Gross National Product as found in the Survey of Current Business issued by the United States Department of Commerce. The inflation factor is the result of dividing the latest published annual deflator by the deflator for the previous year. The commissioner shall inform the owner or operator of the inflation factor needed to adjust cost estimates. Adjustments must be made by multiplying the latest cost estimate by the inflation factor. The result is the adjusted cost estimate.

In addition to any yearly update made under this subpart, the owner or operator must revise the cost estimates whenever a change in site conditions increases the cost of closure, postclosure care, or corrective action. The revised cost estimates must be adjusted for inflation as specified in this subpart.

Subp. 3.

Record retention.

The owner or operator must keep at the facility during the operating life of the facility: the latest cost estimates prepared in accordance with subpart 2, and, when the estimates have been adjusted in accordance with subpart 2, the latest adjusted cost estimates.

History:

13 SR 1150; 15 SR 2308

Published Electronically:

April 24, 2023

Official Publication of the State of Minnesota

Revisor of Statutes